Table Of Content

Bi-weekly payments equate to one extra payment each year and 51 fewer months on a 30-year loan. Before signing, confirm a bi-weekly payment option with your lender. Typically, it is worthwhile to refinance if the reduction in total interest expected to be paid over the life of the loan is greater than the cost of acquiring the loan.

year mortgage rate advances, +0.20%

Reviewing your credit reports can give you an idea of the refinance rates for which you're likely to qualify. It's also an opportunity to check for errors so you can dispute them and possibly have them removed before you apply for a loan. If cash-out refinancing is your goal, you'll want to determine your loan-to-value (LTV) ratio. That's how much you still owe on the home versus what it's worth.

Gather Documents And Apply

However, the shorter the lock, the better the rate, so get your paperwork in quickly and stay in contact with your loan officer during the refinance process. It depends not only on your own current financial situation, but also on the general financial climate. When it’s volatile — as it has been since 2022, with interest rates moving up — you might want to hold off on a major move. Gather recent pay stubs, federal tax returns, bank/brokerage statements and anything else your mortgage lender requests.

What do I need to do for the homeowners insurance verification?

Like when you applied for your first mortgage, you’ll need to provide several documents to the lender when you apply for refinancing. Mortgage lenders typically require a home appraisal (similar to the one done when you bought your house) to determine its current market value. A professional appraiser will assess your home based on criteria and comparisons to the value of similar homes recently sold in your neighborhood. The lender pays the money to the home seller, then you pay the lender back, typically monthly.

Refinance calculator

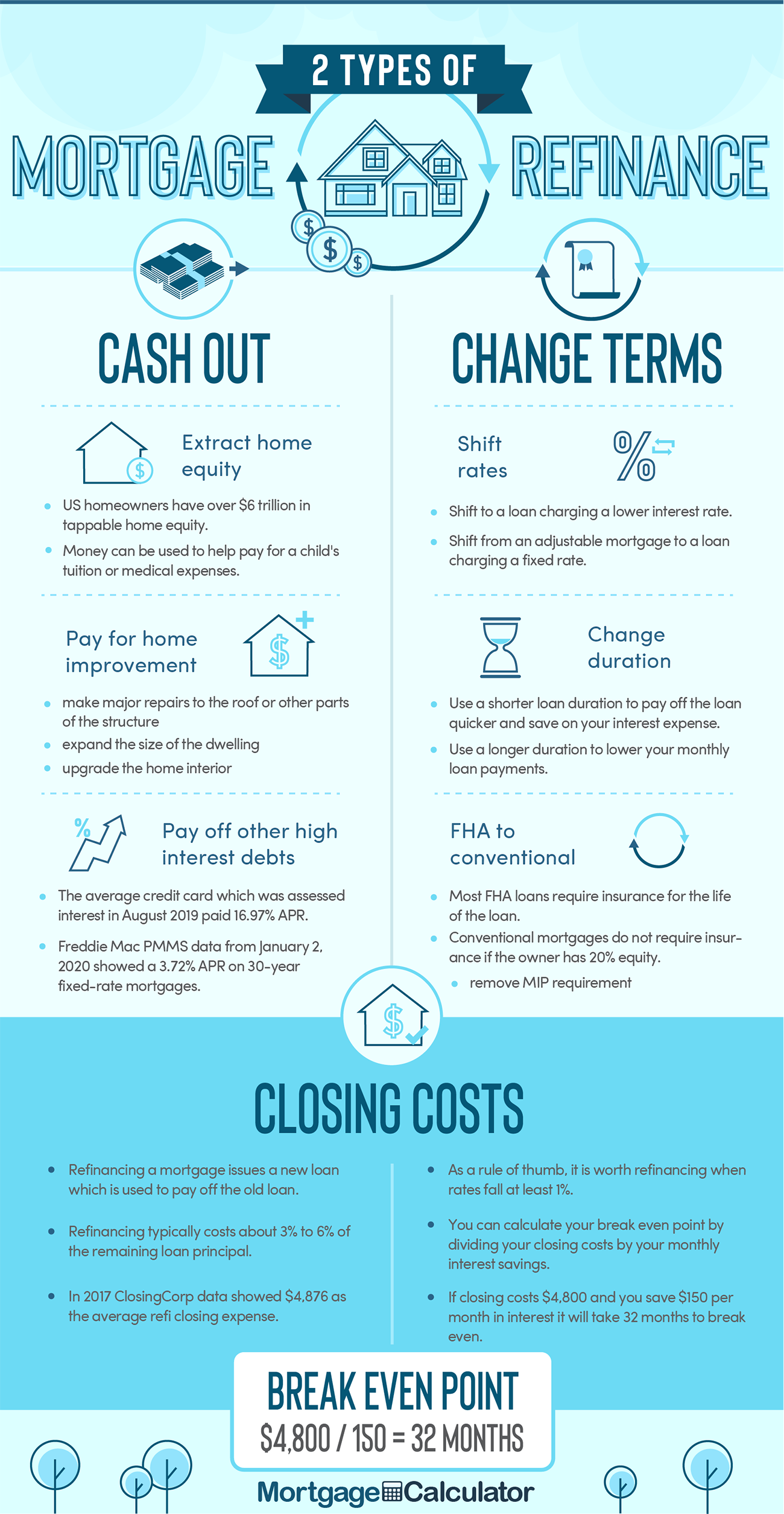

You can expect closing costs to equal around 3% – 6% of your refinance loan amount. Make sure you can pay these costs before you apply, or inquire about having your lender roll them into your refinance loan so you don’t have to pay them upfront. A preapproval is based on a review of income and asset information you provide, your credit report and an automated underwriting system review. The issuance of a preapproval letter is not a loan commitment or a guarantee for loan approval. Preapprovals are not available on all products and may expire after 90 days. Average refinance closing costs range between 2%-6% of the loan amount.

Deciding if a mortgage refinance is right for you

When to Consider Refinancing Your Mortgage - Business Insider

When to Consider Refinancing Your Mortgage.

Posted: Tue, 12 Mar 2024 07:00:00 GMT [source]

Keep in mind that you’ll likely have to make a higher monthly payment over the course of the new loan. You’ll need to think through a number of factors when deciding if you should refinance. Consider market trends – including current interest rates – and your financial situation (especially your credit score). It’s a good idea to use a mortgage refinance calculator to figure out your break-even point after accounting for refinancing expenses. If you’re refinancing to take cash out, for example, then the value of your home determines how much money you can get. After you’ve chosen a refinance type, it’s time to choose a mortgage lender.

There are several reasons to refinance, including getting cash from your home, lowering your payment and shortening your loan term. There are several reasons why you might choose to refinance your mortgage, such as if you can qualify for a lower interest rate or pay off your mortgage faster. But before you proceed, it’s important to understand the potential downsides as well as exactly what the entire process entails. When you refinance your mortgage, you’re not redoing it; you’re replacing your current mortgage with an entirely new loan.

How to Decide if You Should Refinance in 2024 - CNET

How to Decide if You Should Refinance in 2024.

Posted: Wed, 21 Feb 2024 08:00:00 GMT [source]

For example, say you started with a 30-year loan but can now afford a higher mortgage payment. You might refinance to a 15-year term to get a better interest rate and pay less interest overall. Your lender will verify the details of the property, like when you bought your home. The refinance appraisal is a crucial part of the process because it determines what options are available to you. Because refinance lenders check your credit, you might see a temporary dip in your score of up to five points. Try to do all of your shopping within a 14-day period to avoid a bigger drop because of multiple credit inquiries.

This can give you more room in your monthly budget, long-term cost savings or, ideally, both. Once your home appraisal comes back (if you need one), your loan will be reviewed by an underwriter for final approval. The lender will order a payoff statement from your current lender and update your homeowners insurance to reflect the new mortgage company. Once your conditions are clear, you’ll be ready for your refinance closing. Like with other kinds of loans, you’ll typically need a decent credit score to qualify for refinancing. The exact eligibility criteria will depend on the type of loan you choose and the individual lender, with some having less stringent qualifications than others.

At this stage, you should be close to sealing the deal on a new loan. Your lender may offer you the opportunity to lock your rate for a fee. This means your interest rate won't change before you close on the loan. Whether it makes financial sense to lock in your rate depends on what's happening with interest rates. If rates are volatile or appear poised to rise, paying for a rate lock could be worth it.

Apply online for expert recommendations with real interest rates and payments. The closing for a refinance is faster than the closing for a home purchase. The closing is attended by the people on the loan and title and a representative from the lender or title company. Just like when you bought your home, you must get a refinance appraisal before you refinance. Your lender orders the appraisal, the appraiser visits your property, and you receive a professional opinion of your home’s value. The lender will request the lock and send you an updated loan estimate confirming the lock.

This is important to know early in the process because lenders may cap the amount of equity you can withdraw based on your LTV. If refinancing won't provide as much cash as you're hoping for, you may want to wait until you've accumulated more equity. Refinancing a mortgage means taking out a new home loan to replace an existing loan.

In 2020, mortgage refinance activity reached a level not seen since 2003, as homeowners scrambled to take advantage of historically low rates. But before you decide to refinance, here's what you should know. One place to start your search is with a list of the best mortgage refinance lenders. You can also expand your search to small or midsize credit unions, regional banks and local banks. Common reasons to refinance your home are to lower your interest rate, shorten your loan term, lengthen your loan term or reduce your monthly payment.

Title insurance is protection against loss that arises from problems connected to the title of your property. The coverage includes liens, fraud, undisclosed heirs, unpaid real estate taxes and more. If you're worried about qualifying for a refinance with your current credit, there are strategies for refinancing with bad credit. Different lenders have slightly different refinance requirements. To make it simple, we’ve summarized the general requirements to refinance a mortgage in the table below.

When you shorten the loan term — from 30 years to 15 years, for example — you almost always end up with a higher monthly payment, even with a lower interest rate. That's because you'll pay principal (the amount you borrowed) over fewer months. A short refinance can be a great option for borrowers who have defaulted on their mortgage loan payments and are at risk of foreclosure. A reverse mortgage is technically a type of refinancing option for borrowers over the age of 62 with sufficient equity in their homes. Borrowers who switch to a reverse mortgage don't have to make payments on their loan while they’re alive.

No comments:

Post a Comment